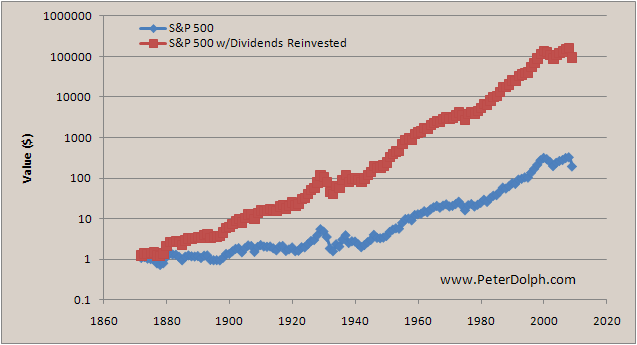

Much ado has been made about the prudence of long-term investing in the stock market. Mutual funds are often quoted as having 10%/year long-term growth. Burton G. Malkie (author of A Random Walk Down Wall Street) recommends the average investor would do better by purchasing an unmanaged index fund (specifically the Wilshire 5000 for the U.S. market) over a managed mutual fund. This post will track stock market returns by considering historic S&P 500 data from 1871-2009 pieced together by Robert Shiller (author of Irrational Exuberance). I say pieced together because the modern S&P 500 didn't exist until 1957.

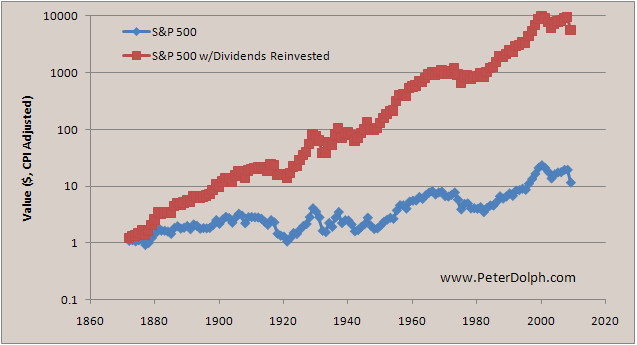

The below graph is somewhat more interesting because it has been CPI-adjusted. All values are given in 2009 dollars.

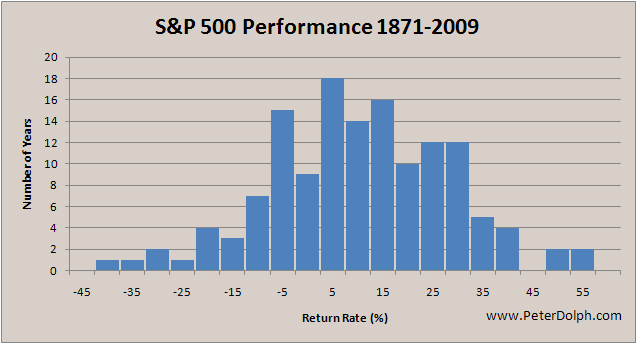

Once again, the top curve (red) shows the investment history with dividends reinvested, while the bottom curve (blue) is an inflation-adjusted price history of the index. In this case the index has an average return rate of 1.80%/year, while the dividends-reinvested investment has a return rate of 6.41%/year. The following histogram shows the spread in returns for the inflation-adjusted, dividends-reinvested case:

If history repeats itself, a long-term investor can expect to earn an inflation-adjusted 6.41%/year in the S&P 500. After a 15% capital-gains tax, the investor will be left with a 5.45%/year investment (some fraction of which will be lost to a financial adviser/firm). At 5.45%/year, the investment should double in just under 13 years (the doubling time is given by 100%*ln(2)/investment rate). This 5.45%/year is significantly less than the 10%/year I seem to remember mutual fund advisers quoting. This leads me to believe that the real way to get rich (other than, you know, earning money) is to maximize your personal savings rate (the American average being 6.98%/year).

Copyright © 2010 Peter Dolph

2 comments:

You need to account for risk in order to see how mutual funds can offer a 10% return. The S&P500 is a (somewhat narrow) market tracking investment index, and so will have close to the minimum risk level (variance of returns) that is possible in the marketplace. It is very much possible to yield a 10% return in the market using a mutual fund, but the underlying risk on that fund must necessarily be higher than the S&P500. In the end, it is a question of investor risk preference - if you like risk, you can (potentially) earn a higher reward (while accepting that you may also "earn" higher losses); otherwise, there are plenty of low-risk (corporate bonds) or risk-free (US T-Bills) investments out there that earn small returns.

Inflation affects all investments denominated in the same currency. So when you're deciding how to invest your money, inflation only matters if you're picking a currency. So the after-inflation return might be 4%, but the after-inflation return of a savings account is 0%.

It is a good thing to remember, though, when planning for retirement. Your return might be 10%/annum (stock market has done slightly better in the past 50 years than in 1870-1920 I think), prices will go up by 4%/annum, giving you a real return of 6%. So you need to save enough to compensate.

Post a Comment